Login

Login

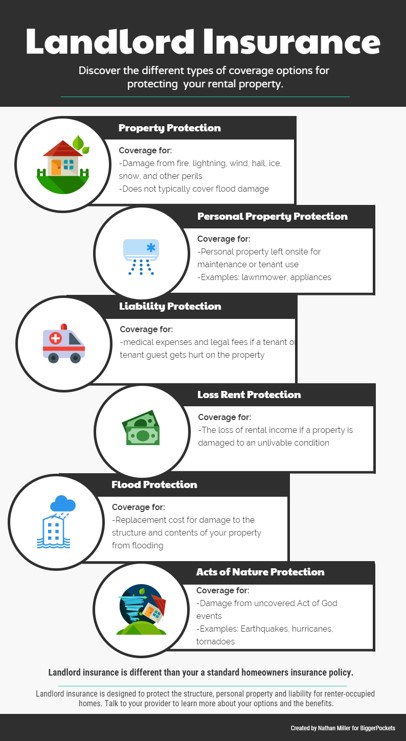

1. Property Protection

Insurance policies designed for rental dwellings provide property insurance coverage for damage to the home from fire, lightning, wind, hail, ice, snow, and other types of covered incidents. Standard landlord policies typically do not cover flood damage; you will have to take out a separate flood insurance policy (see below).

It’s important to note that property protection is often referred to as “dwelling coverage” by insurance policy providers.

2. Personal Property Protection

Landlord policies cover personal property left on-site for maintenance or tenant use, such as appliances and lawnmowers. Landlord policies do not cover tenant property; your tenants will need to have their own renters insurance policy to cover damaged tenant property.

Landlords can require that their tenants get renter’s insurance as a condition of the lease. One of the major benefits of renter’s insurance is avoiding disputes about who will replace a renter’s personal property if damage occurs.

3. Liability Protection

Landlord policies can include liability coverage. If one of your tenants or a guest gets hurt on the property, liability protection covers legal fees and medical expenses.

4. Rent Loss Protection

If your property is damaged to the point where it is uninhabitable, your landlord policy will cover the lost rent and pay you the amount of money you would have made in rental income. Rent loss insurance helps you continue to make mortgage payments when a tenant cannot occupy the home.

We are seeing loss of rent insurance becoming extremely valuable to investors in California whose homes were destroyed in the wildfires. Due to the construction labor shortage, rebuilding efforts will be significantly delayed and this type of insurance will help mitigate the financial loss of a vacant property during that time.

5. Flood Protection

Flood insurance policies are run by the federal government through the National Flood Insurance Program (NFIP) and must be purchased in addition to your landlord insurance policy. Your flood insurance policy can include coverage for the building, contents, and replacement costs. Your insurance agent can help you purchase a flood insurance policy from NFIP.

6. Acts of Nature Protection

Your dwelling coverage might be limited to certain types of damage—and exclude other types of peril. Earthquakes, hurricanes, and tornadoes are acts of nature that are not always covered by your standard landlord insurance policy. If you live in an area at risk for earthquakes, hurricanes, or tornadoes, talk to your provider to add additional peril protections.

Acts of nature protection is sometimes referred to as “acts of God” by your policy provider.

Related: Property Insurance: Why Coverage Gets Dropped & How to Handle It

7. Cash Value vs. Replacement Cost

When you design your landlord insurance policy, you need to consider cash value versus replacement cost when filing a claim.

When repairing or rebuilding damaged property, an actual cost value policy will pay you the actual cost minus the depreciation value of damaged items. For example, if you purchased an appliance for the property that gets damaged in a fire, your insurer will value the actual cost of that appliance now (with depreciation) and pay you that amount. So, if you bought a washing machine for $600 three years ago, the insurer will depreciate the value of the washing machine to reflect its current value at 3 years old and pay you that amount—not the amount it would cost to buy a new washing machine.

Replacement value will pay you the value equal to replacing a damaged item. Compared to actual cash value, replacement value will get a new item at no out-of-pocket cost to you. If you are willing to pay the difference out of pocket, actual cost coverage will be fine. But if you would rather insurance take care of everything, replacement cost coverage is the way to go. Understandably, replacement cost coverage will cost more than actual cost coverage.

Landlord Insurance Options

As you can see, there are many things that must be considered when choosing your landlord insurance policy. It is important to read the policy carefully, discuss options with your agent and ensure that you are fully protected. As we’ve all seen recently, just about anything can happen, so it’s a good idea to be prepared with the proper insurance policy to cover your investment and meet your needs.